Can You Short Sale a Reverse Mortgage?

Yes, you may be able to short sale a reverse mortgage if the home is worth less than the reverse mortgage balance. This is especially common when the loan balance has grown over time, the property value has dropped, the borrower has passed away, or the borrower needs to move out of the home and there is not enough equity to pay off the reverse mortgage through a normal sale.

A reverse mortgage short sale is different from a traditional short sale because many reverse mortgages are Home Equity Conversion Mortgages, also called HECMs, which are insured by the Federal Housing Administration. Because of that, there are specific rules for selling, payoff approval, appraised value, mortgage insurance, heirs, and what happens if the reverse mortgage balance is higher than the value of the home.

If you are asking, “Can I short sale a reverse mortgage?” or “How do I sell a home with a reverse mortgage if there is no equity?” the answer is often yes, but the process must be handled correctly. The lender, servicer, and possibly HUD must approve the terms before the sale can close.

Quick Summary

- A reverse mortgage can usually be paid off through a normal sale if the home has enough equity.

- If the reverse mortgage balance is higher than the home value, the property may need to be sold through a reverse mortgage short sale.

- Most reverse mortgages are HECM loans insured by FHA.

- HECM reverse mortgages are generally non-recourse, which means the borrower or heirs usually do not owe more than the value of the home.

- If a HECM loan is due and payable and the home is underwater, the home may be sold for 95% of its appraised value in certain situations.

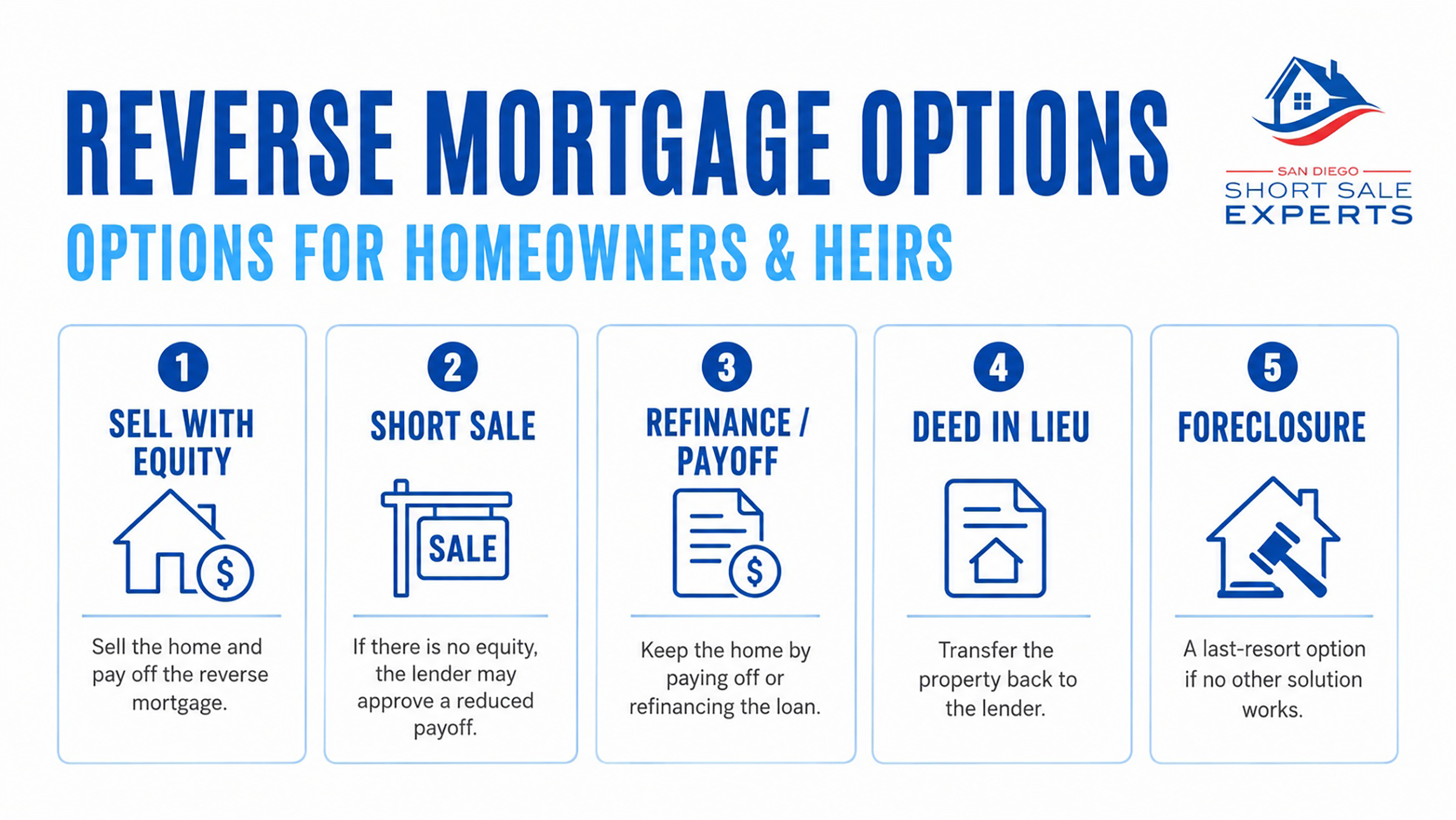

- Heirs may have options to sell the home, keep the home, refinance the loan, complete a deed in lieu, or allow the lender to foreclose.

- A reverse mortgage short sale should be handled by someone familiar with short sales, reverse mortgage servicers, lender approval letters, HUD rules, title issues, and foreclosure timelines.

What Is a Reverse Mortgage Short Sale?

A reverse mortgage short sale is a lender-approved sale where a home with a reverse mortgage is sold for less than the full amount owed on the loan.

In a traditional sale, the home sells for enough money to pay off the mortgage balance, closing costs, escrow fees, title fees, real estate commissions, and any other liens or approved selling expenses. If there is money left over, that remaining equity goes to the homeowner or the estate.

In a reverse mortgage short sale, there is not enough equity to pay everything in full. The sale proceeds are “short” of the total amount needed to satisfy the reverse mortgage payoff and selling costs. Because of that shortage, the lender or loan servicer must approve the sale before the property can close.

This type of situation often comes up when:

- The reverse mortgage balance has grown over time.

- Interest, fees, and mortgage insurance have been added to the loan balance.

- The home value has not increased enough to keep up with the loan balance.

- The borrower has passed away.

- The borrower has moved into assisted living, a nursing home, or with family.

- Property taxes, homeowners insurance, HOA dues, or maintenance obligations have not been kept current.

- The property is in default or foreclosure.

- The heirs do not want to keep the home.

- The estate cannot afford to pay off the reverse mortgage.

If you are not familiar with short sales in general, you may also want to read our guide on what a short sale is.

Can You Short Sale a Reverse Mortgage?

Yes, it is possible to short sale a reverse mortgage. The key issue is whether the lender or loan servicer will approve the sale terms.

If the home has enough equity, the process may be closer to a regular sale. The reverse mortgage is paid off at closing, the lien is released, and any remaining proceeds go to the homeowner or estate.

If the home does not have enough equity, the sale may need to be handled as a short sale. In that case, the lender or servicer reviews the offer, the property value, the payoff amount, the closing costs, and the required documentation before issuing a written approval.

For many homeowners and heirs, a short sale may be a more controlled option than letting the home go through foreclosure. It allows the property to be marketed, a buyer to be selected, the sale terms to be reviewed, and the transaction to close through escrow instead of being completed through a foreclosure sale.

However, a reverse mortgage short sale is not automatic. The servicer must review the file, and the approval terms must be clearly documented before closing. For a broader overview of how lender-approved short sales work, read our guide to the short sale process.

Why a Reverse Mortgage May End Up With No Equity

Reverse mortgages work differently than traditional mortgages.

With a traditional mortgage, the homeowner usually makes monthly principal and interest payments. Over time, the loan balance may go down if payments are made as agreed.

With a reverse mortgage, the borrower may not be required to make monthly mortgage payments. Instead, the loan balance can grow over time as interest, fees, mortgage insurance premiums, and loan advances are added to the balance.

That can create a situation where the home has little or no equity, especially if:

- The reverse mortgage was taken out years ago.

- The borrower used a large portion of the available loan proceeds.

- Interest rates increased.

- The home did not appreciate as expected.

- Property condition declined.

- The local market softened.

- The home needs repairs before it can sell for top value.

- The borrower lived in the home for many years after taking out the reverse mortgage.

This does not always mean the borrower or heirs must pay the shortage out of pocket. Many reverse mortgages are non-recourse, which means the lender’s recovery is generally limited to the home itself. However, the exact outcome depends on the loan type, approval terms, state law, title issues, and the facts of the file.

What Happens When a Reverse Mortgage Is More Than the Home Is Worth?

When a reverse mortgage balance is higher than the home value, the home is considered underwater.

| Item | Example Amount |

|---|---|

| Estimated home value | $600,000 |

| Reverse mortgage payoff | $675,000 |

| Estimated selling costs | $45,000 |

| Total needed for normal sale | $720,000 |

| Estimated shortage | $120,000 |

In this example, the home cannot be sold through a normal sale unless someone brings money to closing or the lender approves a reduced payoff. If the seller, borrower, heirs, or estate cannot or do not want to pay the shortage, a reverse mortgage short sale may be the solution.

The lender or servicer will typically review the current market value, the appraised value, the reverse mortgage payoff, and the sale offer. If the offer and closing terms meet the required guidelines, the lender may approve the sale even though the proceeds are less than the full balance owed.

The Consumer Financial Protection Bureau explains that if a reverse mortgage loan balance is more than the value of the home, the borrower or heirs may not have to pay the difference in certain HECM situations.

The Reverse Mortgage 95% Rule

One of the most important concepts in a reverse mortgage short sale is the 95% appraised value rule for many FHA-insured HECM loans.

In many HECM situations, if the loan is due and payable and the reverse mortgage balance is higher than the value of the home, the property may be sold for 95% of the current appraised value. The remaining balance may be covered by mortgage insurance.

This rule can be extremely important for homeowners, heirs, and estates. It may allow the home to be sold even when the reverse mortgage payoff is higher than the home’s market value.

| Item | Example Amount |

|---|---|

| Reverse mortgage payoff | $700,000 |

| Current appraised value | $600,000 |

| 95% of appraised value | $570,000 |

| Potential approved sale price | $570,000 or more |

| Shortage compared to payoff | $130,000 |

In this example, the home may be sold for less than the full reverse mortgage payoff if the lender approves the sale and the transaction meets the required guidelines. The seller should not assume this will happen automatically. The payoff, appraisal, sale price, closing costs, and approval letter all need to be reviewed carefully.

For more information, review the CFPB’s explanation of what happens when selling a home with a reverse mortgage and the CFPB’s guidance on whether heirs can keep or sell a home after a reverse mortgage borrower dies.

Short Sale Example With a Reverse Mortgage

Let’s say a homeowner has a reverse mortgage and needs to move out of the property.

The home is worth approximately $500,000, but the reverse mortgage payoff is $575,000. The seller also has closing costs, escrow fees, title fees, and real estate commissions that need to be paid at closing.

A normal sale does not work because the sale proceeds are not enough to pay the reverse mortgage in full. The homeowner cannot bring the difference to closing.

In this situation, the steps may look like this:

- The homeowner contacts a short sale professional.

- The reverse mortgage payoff is requested.

- The estimated market value is reviewed.

- The home is listed for sale.

- A buyer submits an offer.

- The seller accepts the offer subject to lender approval.

- The short sale package is submitted to the reverse mortgage servicer.

- The servicer reviews the offer, value, closing costs, and required documents.

- The servicer may order or review an appraisal.

- The lender approves, counters, denies, or requests more information.

- If approved, the sale moves forward to closing.

- The reverse mortgage lien is released according to the written short sale approval.

The most important detail is that the seller’s acceptance of the buyer’s offer is not enough by itself. The reverse mortgage lender or servicer must approve the short sale before closing.

When a Reverse Mortgage Becomes Due and Payable

A reverse mortgage does not usually require monthly mortgage payments, but it does become due and payable when certain events happen.

Common due-and-payable events include:

- The borrower sells the home.

- The last surviving borrower passes away.

- The borrower no longer lives in the home as their principal residence.

- The borrower moves out permanently.

- The borrower is away from the home for an extended period because of a healthcare facility, nursing home, or assisted living situation.

- The borrower fails to pay property taxes.

- The borrower fails to maintain homeowners insurance.

- The borrower does not keep the property in required condition.

- Other loan obligations are not met.

Once the loan is due and payable, the lender or servicer may require the loan to be repaid. If the home has enough equity, the property can often be sold normally. If there is no equity, a short sale, deed in lieu, refinance, payoff, or foreclosure may need to be evaluated.

The U.S. Department of Housing and Urban Development explains that the HECM is FHA’s reverse mortgage program and that HECM borrowers may remain in the home as long as required obligations, such as property taxes and homeowners insurance, are kept current.

Timing is very important. If a due-and-payable notice or foreclosure notice has already been issued, the homeowner or heirs should act quickly.

Selling a Home With a Reverse Mortgage While the Borrower Is Alive

A borrower can usually sell a home that has a reverse mortgage. The borrower still owns the home, but the reverse mortgage must be paid off when the home is sold.

If the home has equity, the sale may look similar to a traditional sale:

- The home is listed for sale.

- A buyer makes an offer.

- Escrow requests the reverse mortgage payoff.

- The reverse mortgage is paid off at closing.

- Any remaining equity goes to the seller.

If the home does not have equity, the transaction is more complicated. The borrower may need lender approval for a short sale. The lender will review the offer, payoff, value, closing costs, and approval requirements before allowing the sale to close.

A reverse mortgage short sale may be an option when the borrower wants or needs to move but cannot sell the home for enough money to pay off the reverse mortgage in full.

Selling an Inherited Home With a Reverse Mortgage

Reverse mortgage short sales are common after the borrower passes away.

When the last borrower passes away, the reverse mortgage generally becomes due and payable unless there is a qualified co-borrower or eligible non-borrowing spouse who has certain rights to remain in the home.

For heirs, the options may include:

- Sell the home and pay off the reverse mortgage.

- Keep the home by paying off or refinancing the reverse mortgage.

- Sell the home through a short sale if there is no equity.

- Complete a deed in lieu of foreclosure.

- Allow the lender to foreclose.

- Speak with an attorney or probate professional if the estate is involved.

If there is equity, the heirs may be able to sell the home, pay off the reverse mortgage, and keep the remaining proceeds.

If there is no equity, the heirs may still be able to sell the home through a reverse mortgage short sale. In many HECM situations, the home may be sold for 95% of the appraised value if the loan balance is higher than the home value and the servicer approves the transaction.

The heirs should contact the lender or servicer quickly after receiving any due-and-payable notice. Delays can reduce options and increase the risk of foreclosure.

Can a Family Member Buy the Home?

In some reverse mortgage situations, a family member or heir may be able to purchase the home. This is one reason reverse mortgage short sales can be different from traditional short sales.

With a regular short sale, lenders often require an arm’s-length transaction. That usually means the buyer cannot be closely related to the seller and there cannot be a hidden agreement to transfer the property back after closing.

With reverse mortgage situations, especially inherited properties, family members may want to keep the home. A family member may be able to buy the property, but the sale still needs to meet lender, servicer, HUD, title, escrow, and financing requirements.

Before assuming a family purchase will be approved, the parties should confirm:

- The type of reverse mortgage.

- Whether the loan is FHA-insured HECM.

- The current payoff balance.

- The lender’s required payoff amount.

- Whether an appraisal has been completed.

- Whether the 95% rule applies.

- Whether the buyer can qualify for financing.

- Whether probate or estate authority is required.

- Whether title can be transferred properly.

- Whether all heirs agree to the sale.

A family purchase can be possible, but it needs to be handled carefully.

Reverse Mortgage Short Sale Process: Step-by-Step

The reverse mortgage short sale process usually includes the following steps.

1. Review the Reverse Mortgage Payoff

The first step is to request or review the current payoff from the reverse mortgage servicer. The payoff should show the loan balance, interest, fees, mortgage insurance, and any other amounts included in the debt.

2. Estimate the Current Market Value

Next, the home’s current value needs to be reviewed. This may include comparable sales, active listings, property condition, repair issues, and local market trends.

The value review is important because the lender will want to know whether the offer represents fair market value.

3. Determine Whether There Is Equity

The estimated sale price should be compared against the reverse mortgage payoff and selling costs.

If there is enough equity, a regular sale may be possible. If there is not enough equity, a short sale may be needed.

4. Identify the Decision Maker

This is especially important after the borrower passes away. The person signing the listing agreement and sale documents must have legal authority to sell the property.

Depending on the situation, this may involve:

- The borrower.

- A surviving co-borrower.

- A trustee.

- An executor.

- An administrator.

- A personal representative.

- An heir with proper authority.

- A court-approved representative.

If probate is involved, the estate should speak with a qualified probate attorney.

5. Contact the Reverse Mortgage Servicer

The servicer needs to know that the borrower, heirs, or estate are working on a sale. Communication is important, especially if a due-and-payable notice or foreclosure timeline has started.

6. List the Home for Sale

The property should usually be listed at a realistic market value. Overpricing can waste valuable time. Underpricing can create lender approval problems.

The listing agent should understand that any accepted offer will likely be subject to reverse mortgage short sale approval.

7. Accept a Buyer’s Offer Subject to Lender Approval

The seller may accept an offer, but the contract should make clear that the sale is subject to lender or short sale approval. The buyer should understand that the approval process can take longer than a traditional sale.

8. Submit the Short Sale Package

The short sale package may include:

- Purchase contract.

- Listing agreement.

- Estimated settlement statement or net sheet.

- Buyer proof of funds or lender approval.

- Payoff information.

- Hardship or explanation letter, if required.

- Death certificate, if applicable.

- Trust, probate, or estate documents, if applicable.

- Authorization forms.

- Property condition information.

- Required lender or servicer forms.

The exact package depends on the servicer and file. For more information about short sale documentation, visit our page on how to qualify for a short sale.

9. Respond to Lender Questions and Valuation Issues

The lender may order an appraisal or valuation. If the lender’s value is too high, the agent may need to provide comparable sales, repair estimates, photos, inspection information, and market data.

10. Review the Short Sale Approval Letter

The written approval letter is one of the most important documents in the entire transaction. It should be reviewed carefully before closing.

The approval letter should confirm:

- Approved sale price.

- Approved closing costs.

- Approved commission.

- Closing deadline.

- Required payoff.

- Whether the remaining balance is waived, satisfied, insured, or otherwise handled.

- Whether the seller must contribute funds.

- Whether any relocation or incentive funds are approved.

- Any restrictions on buyers, resale, or parties.

- Any required signatures.

Do not close based on verbal approval.

11. Close Escrow

Once the lender has approved the short sale, escrow can move toward closing. The sale proceeds are applied according to the approval letter and settlement statement. After closing, the reverse mortgage lien should be released as required by the approved terms.

What the Lender Will Review

In a reverse mortgage short sale, the lender or servicer may review:

- Current appraised value.

- Purchase price.

- Loan payoff.

- Property condition.

- Closing costs.

- Commission.

- Tax or HOA amounts.

- Buyer qualifications.

- Whether the sale is arm’s length or family-related.

- Whether the borrower is living, deceased, or moved out.

- Whether the loan is due and payable.

- Whether foreclosure has started.

- Whether probate or legal authority is in place.

- Whether HUD or mortgage insurance guidelines apply.

The lender’s goal is to confirm that the transaction meets investor, FHA, HUD, mortgage insurance, servicing, and title requirements.

Reverse Mortgage Short Sale vs. Foreclosure vs. Deed in Lieu

A reverse mortgage short sale is not the only option. Homeowners and heirs should compare all available choices.

| Option | How It Works | Best For | Potential Concern |

|---|---|---|---|

| Traditional Sale | Home sells for enough to pay off the reverse mortgage and costs. | Homes with equity. | Not possible if the payoff is higher than value. |

| Reverse Mortgage Short Sale | Lender approves a sale for less than the full payoff. | Homes with no equity or negative equity. | Requires approval and documentation. |

| Deed in Lieu | Owner or estate transfers the property back to the lender. | Heirs who do not want to sell or keep the home. | May not be best if there is equity or title issues. |

| Foreclosure | Lender completes the legal foreclosure process. | Last resort when no other option works. | Loss of control, deadlines, possible credit or estate consequences. |

| Refinance or Payoff | Borrower or heirs pay off the reverse mortgage. | Heirs who want to keep the home. | Requires cash or financing ability. |

A short sale is often worth exploring before foreclosure because it may give the homeowner or heirs more control over the process. You can also review our full guide to short sale vs. foreclosure and our article on alternatives to foreclosure.

Pros and Cons of a Reverse Mortgage Short Sale

Potential Benefits

A reverse mortgage short sale may:

- Help avoid foreclosure.

- Allow the home to be sold even if there is no equity.

- Give the homeowner or heirs more control over the sale.

- Allow the property to be marketed to regular buyers.

- Help resolve a due-and-payable reverse mortgage.

- Allow the estate to move forward.

- Reduce stress for heirs who do not want to keep the home.

- Avoid leaving the property vacant for an extended period.

- Allow a family member or heir to potentially purchase the home in some situations.

Potential Drawbacks

A reverse mortgage short sale may also involve:

- Lender approval delays.

- Strict valuation requirements.

- A longer escrow timeline.

- Required documentation.

- Probate or title complications.

- Limited flexibility on closing costs.

- No proceeds to the seller if there is no equity.

- Possible tax, legal, or credit consequences.

- Risk of foreclosure if the process starts too late.

The best option depends on the loan, property value, timeline, borrower status, heirs, estate issues, and lender requirements.

Common Mistakes to Avoid

Reverse mortgage short sales can go wrong when homeowners, heirs, agents, or buyers do not understand the process.

Waiting Too Long

If a due-and-payable notice or foreclosure notice has been issued, time matters. Waiting too long can make approval harder and may reduce the ability to request extensions.

Assuming the Home Cannot Be Sold

Many heirs assume that if the reverse mortgage balance is higher than the home value, the only option is foreclosure. That is not always true. A short sale may still be possible.

Listing the Home Without Understanding the Payoff

Before listing, it is important to understand the reverse mortgage payoff, estimated value, selling costs, and whether the home is likely to be a short sale.

Overpricing the Home

Overpricing can cause the property to sit on the market while the foreclosure timeline continues. A realistic price strategy is important.

Accepting an Offer Without Buyer Education

The buyer needs to understand that lender approval is required and that the timeline may be longer than a normal sale.

Not Reviewing the Approval Letter

Never assume the remaining balance is handled correctly. The approval letter should be reviewed before closing. You can learn more about this issue in our article on what happens to the balance after a short sale.

Ignoring Probate or Authority Issues

If the borrower has passed away, the person signing documents must have authority to sell the home. Probate, trust, title, or estate issues should be addressed early.

Not Getting Professional Advice

A reverse mortgage short sale may involve tax, legal, estate, probate, foreclosure, and credit issues. Sellers and heirs should consult qualified professionals when needed.

Tax, Legal, and Probate Considerations

A reverse mortgage short sale may involve tax and legal questions. Every situation is different.

Important issues may include:

- Whether the loan is a HECM reverse mortgage.

- Whether the loan is non-recourse.

- Whether the borrower is living or deceased.

- Whether the estate is in probate.

- Whether a 1099-C may be issued.

- Whether mortgage insurance covers the unpaid balance.

- Whether there are other liens on title.

- Whether property taxes, HOA dues, or municipal liens are owed.

- Whether all heirs agree to the sale.

- Whether an attorney, CPA, or probate professional should be involved.

San Diego Short Sale Experts can help explain the real estate and short sale process, but we do not provide tax or legal advice. Homeowners and heirs should speak with a qualified CPA, tax attorney, estate attorney, or foreclosure attorney about their specific situation.

For related information, review our pages on taxes after a short sale, credit after a short sale, and how much a short sale costs.

When to Talk to a Short Sale Expert

You should speak with a short sale professional as soon as possible if:

- You have a reverse mortgage and need to sell.

- The home has little or no equity.

- The reverse mortgage payoff is higher than the home value.

- You inherited a home with a reverse mortgage.

- The borrower has passed away.

- The borrower moved into assisted living or a nursing home.

- You received a due-and-payable notice.

- You received a foreclosure notice.

- You are unsure whether the 95% rule applies.

- You want to compare short sale, deed in lieu, foreclosure, and refinance options.

- You are an heir and do not know what to do next.

- A family member wants to buy the home.

- The property needs repairs and cannot sell for the payoff amount.

San Diego Short Sale Experts helps California homeowners and heirs understand their options when a reverse mortgage property has little or no equity. We can help review the estimated value, reverse mortgage payoff, sale options, short sale process, timelines, buyer strategy, and next steps.

There is no cost or obligation to have a confidential conversation with our team.

Call San Diego Short Sale Experts at 619.777.6716 or contact us online to discuss your situation.

Frequently Asked Questions About Short Selling a Reverse Mortgage

Can you short sale a reverse mortgage?

Yes, a reverse mortgage may be eligible for a short sale if the home is worth less than the loan payoff and the lender or servicer approves the sale. The approval process depends on the loan type, current value, payoff amount, property status, and required documentation.

Can I short sale a reverse mortgage if I am not behind on anything?

Yes. Since you do not make payments on a reverse mortgage, this is not a factor as it is in a traditional mortgage. A reverse mortgage short sale may be considered when the borrower needs to sell but the home does not have enough equity to pay off the loan in full. However, the lender or servicer must review and approve the sale.

How do I sell a home with a reverse mortgage if there is no equity?

If there is no equity, you generally need to determine the payoff amount, estimate the home’s value, contact the reverse mortgage servicer, list the property, accept an offer subject to lender approval, and submit a short sale package. The lender must approve the reduced payoff before closing.

What happens if my reverse mortgage is more than my home is worth?

If the reverse mortgage balance is more than the home value, the home may be underwater. For many HECM reverse mortgages, the borrower or heirs may not have to pay the difference if the home is sold according to the applicable rules and the lender approves the transaction.

What is the reverse mortgage 95% rule?

In many HECM situations, if the loan is due and payable and the loan balance is higher than the home value, the home may be sold for 95% of the current appraised value. The remaining balance may be covered by mortgage insurance. The servicer should confirm the requirements for the specific loan.

Do heirs have to pay back a reverse mortgage?

Heirs do not automatically have to pay the reverse mortgage from their personal funds. If they want to keep the home, they may need to pay off or refinance the loan. If they do not want to keep the home, they may be able to sell it, short sell it, complete a deed in lieu, or allow the lender to foreclose.

Can heirs sell a home with a reverse mortgage?

Yes, heirs may be able to sell a home with a reverse mortgage, but the loan must be resolved through the sale. If there is equity, the reverse mortgage is paid off and the remaining proceeds may go to the estate or heirs. If there is no equity, a short sale may be needed.

Can a family member buy a home with a reverse mortgage?

In some cases, yes. A family member or heir may be able to purchase the home, but the sale must meet lender, servicer, HUD, escrow, title, and financing requirements. The rules can be different from a standard short sale, so the file should be reviewed carefully.

Is a reverse mortgage short sale better than foreclosure?

A short sale may be better than foreclosure in many situations because it gives the homeowner or heirs more control over the sale and may help resolve the property before foreclosure is completed. However, the best option depends on equity, timeline, estate issues, legal advice, tax advice, and lender approval.

Is a deed-in-lieu better than a reverse mortgage short sale?

A deed in lieu may be simpler if there is no equity and the heirs do not want to sell or keep the property. However, a short sale may be better if there is a buyer, the property can be sold, a family member wants to purchase it, or the estate wants more control over the process.

How long does a reverse mortgage short sale take?

A reverse mortgage short sale can take several weeks to several months, depending on the lender, servicer, appraisal, buyer, title issues, probate issues, foreclosure status, and documentation. Starting early is important.

Will the seller receive money from a reverse mortgage short sale?

If there is no equity, the seller or heirs usually should not expect to receive proceeds from the sale. The sale proceeds are applied toward the reverse mortgage and approved closing costs according to the lender’s approval letter.

Are there tax consequences after a reverse mortgage short sale?

There may be tax consequences depending on whether debt is canceled, whether the loan is non-recourse, whether mortgage insurance covers the shortage, whether the borrower is living or deceased, and how the transaction is reported. Speak with a qualified CPA or tax attorney before closing.

Do I need an attorney for a reverse mortgage short sale?

An attorney is not always required to list the home, but legal advice may be important if the borrower has passed away, probate is involved, foreclosure has started, multiple heirs disagree, title is unclear, or there are questions about liability, taxes, or estate authority.

What should I do first if I need to short sale a reverse mortgage?

Start by reviewing the reverse mortgage payoff, estimated home value, property condition, foreclosure status, and who has authority to sell the property. Then speak with a short sale expert who understands reverse mortgage approvals and can help you compare your options.

Need Help Selling a Home With a Reverse Mortgage?

If the reverse mortgage payoff is higher than the value of the home, you may still have options. San Diego Short Sale Experts can help you review the property value, payoff amount, foreclosure status, and whether a reverse mortgage short sale may be possible.

Call 619.777.6716 or contact us online for a confidential consultation.