FHA Loan Short Sale: How to Short Sale an FHA Loan and Avoid Foreclosure

If you have an FHA loan and owe more than your home is worth, an FHA loan short sale may allow you to sell the property, avoid foreclosure, and move forward with more control. FHA short sales are handled through HUD’s Pre-Foreclosure Sale program, often called a PFS. The process is different from a traditional short sale because FHA has specific guidelines, forms, timelines, property value requirements, and approval steps.

At San Diego Short Sale Experts, we help homeowners evaluate FHA short sale options, communicate with the loan servicer, prepare the required documentation, price and market the property, negotiate with the lender, and work toward short sale approval before foreclosure becomes unavoidable.

Quick Answer: Can I Short Sale My FHA Loan?

Yes, you may be able to short sale an FHA loan if your home is worth less than the amount owed and you qualify for HUD’s Pre-Foreclosure Sale program. Your loan servicer will review your situation, property value, financial hardship, foreclosure status, liens, and whether a loan modification or other retention option is realistic before approving an FHA short sale.

Need Help With an FHA Loan Short Sale?

If you are behind on payments, facing foreclosure, or need to sell a home with an FHA loan that is underwater, contact us today. We can review your situation, explain the FHA short sale process, and help determine whether you may qualify.

There is no cost or obligation to speak with us.

Table of Contents

- What Is an FHA Loan Short Sale?

- FHA Short Sale Guidelines

- How the FHA Short Sale Process Works

- What Is FHA Approval to Participate?

- Documents Needed for an FHA Short Sale

- Can an FHA Short Sale Stop Foreclosure in California?

- FHA Short Sale Relocation Assistance

- FHA Short Sale vs. Other Foreclosure Alternatives

- Why Work With San Diego Short Sale Experts?

- FHA Loan Short Sale FAQ

What Is an FHA Loan Short Sale?

An FHA loan short sale is a lender-approved sale of a home with an FHA-insured mortgage when the sale proceeds are not enough to pay off the full mortgage balance and approved selling costs. FHA short sales are commonly handled through HUD’s Pre-Foreclosure Sale program, also known as PFS.

In a traditional sale, the mortgage is paid off in full at closing. In an FHA short sale, the homeowner is asking the loan servicer and HUD to approve a sale for less than the full amount owed. This can be an option when the homeowner has a hardship, the property is underwater, and keeping the home is no longer realistic.

The goal is to complete a controlled sale before foreclosure. This may help the homeowner avoid a completed foreclosure, resolve the FHA mortgage through an approved settlement, and create a clearer path forward.

FHA Short Sale Guidelines

FHA short sale guidelines focus on eligibility, property value, hardship, documentation, arm’s-length sale requirements, and approval from the loan servicer. Every file is different, but the following issues are commonly reviewed.

| FHA Short Sale Issue | What It Means | Why It Matters |

|---|---|---|

| FHA-insured loan | The mortgage must be an FHA-insured loan. | FHA short sales follow HUD-specific rules that are different from conventional short sales. |

| Underwater property | The expected sale price is not enough to pay off the mortgage and approved costs. | The lender and HUD must decide whether accepting less than the full payoff is appropriate. |

| Financial hardship | Examples may include job loss, reduced income, divorce, medical issues, relocation, or increased expenses. | The servicer needs to understand why the homeowner cannot reasonably keep the property. |

| Loss mitigation review | The servicer may review the homeowner for retention options such as repayment, forbearance, or loan modification. | A short sale is usually considered when keeping the home is not realistic or not desired. |

| Approval to Participate | FHA may require the homeowner to be approved for the Pre-Foreclosure Sale program before moving forward. | This is one of the biggest differences between an FHA short sale and many traditional short sales. |

| Arm’s-length sale | The buyer cannot be a family member, business associate, or favored party. | HUD requires the sale to reflect a legitimate market transaction. |

| Property value review | The lender will evaluate the property value and the buyer’s offer. | The offer must meet FHA/HUD net proceeds requirements or the lender may counter or deny the sale. |

| Junior liens | Second mortgages, HOA liens, tax liens, judgments, or other liens may need to be resolved. | Additional liens can delay or complicate short sale approval. |

How the FHA Short Sale Process Works

The FHA short sale process usually involves a hardship review, property value review, approval to participate, listing the property, submitting an offer, negotiating approval, and closing before the deadline. The exact timeline depends on the servicer, foreclosure status, buyer strength, title issues, and how quickly documents are completed.

1. Review Your Loan, Property Value, and Foreclosure Status

The first step is to confirm that the loan is FHA-insured, estimate the current property value, review the mortgage balance, identify any missed payments, and determine whether a foreclosure date has already been scheduled.

If you are in San Diego or elsewhere in California and have received a Notice of Default or Notice of Trustee Sale, timing is critical. Do not wait until the last few days before a foreclosure sale to explore your options.

2. Determine Whether a Short Sale Makes Sense

An FHA short sale may make sense if the property is underwater, you have a legitimate hardship, you cannot afford to keep the home, and a loan modification or repayment plan is not realistic. A short sale may also be considered when you need to relocate or no longer want to remain in the property.

3. Prepare the FHA Short Sale Package

The servicer will typically request financial documents, hardship information, authorization forms, property information, and supporting documents. Missing paperwork is one of the most common causes of delay, so the file should be complete before submission whenever possible.

4. Obtain FHA Approval to Participate

With an FHA short sale, the homeowner may need to receive Approval to Participate in the HUD Pre-Foreclosure Sale program. This is different from many standard short sales where a homeowner lists the property and submits an offer first.

5. List and Market the Property

The property must be listed with a licensed real estate agent. Proper pricing is important because the lender will compare the buyer’s offer to the approved property value and HUD/FHA net proceeds requirements.

6. Submit the Buyer’s Offer

Once a qualified buyer submits an offer, the purchase contract, buyer proof of funds or pre-approval, estimated settlement statement, listing history, and other required documents are submitted for review.

7. Negotiate the Short Sale Approval

The servicer may approve the offer, counter the offer, request additional documentation, ask for updated financials, question closing costs, or require resolution of liens. A strong file helps reduce avoidable delays.

8. Review the Approval Letter and Close Escrow

If the short sale is approved, the lender will issue a short sale approval letter. This letter should be reviewed carefully before closing because it explains the approved sale terms, deadlines, payoff handling, seller obligations, deficiency language, relocation assistance, and any required contributions.

What Is FHA Approval to Participate?

Approval to Participate is the FHA Pre-Foreclosure Sale approval that allows an eligible homeowner to move forward with the FHA short sale process. It is an important step because it confirms that the servicer has reviewed the file and is allowing the homeowner to attempt a short sale under HUD’s PFS program.

The Approval to Participate may include listing requirements, timelines, property value expectations, minimum acceptable net proceeds, arm’s-length transaction requirements, property maintenance requirements, and instructions for submitting a purchase contract.

Because FHA short sale requirements can be technical, homeowners should not assume that simply listing the property will be enough. The FHA short sale file needs to be handled correctly from the beginning.

Documents Needed for an FHA Short Sale

The exact documents vary by lender and servicer, but most FHA short sale files require financial, hardship, property, and transaction documents. Commonly requested documents include:

- Mortgage statement and FHA loan information

- Hardship letter or hardship explanation

- Recent pay stubs or income documentation

- Recent bank statements

- Tax returns or other financial documents, if requested

- Authorization allowing your short sale specialist to communicate with the servicer

- Listing agreement

- Purchase contract from a qualified buyer

- Buyer pre-approval letter or proof of funds

- Estimated settlement statement

- HOA payoff, property tax information, or other lien information

- Repair estimates or supporting market data, if value is disputed

Before You Submit FHA Short Sale Paperwork

Incomplete or inconsistent documents can slow down the review and may create problems if there is a pending foreclosure date. We can help you understand what may be needed before the FHA short sale file is submitted.

There is no cost or obligation to speak with us.

Can an FHA Short Sale Stop Foreclosure in California?

An FHA short sale may help avoid foreclosure, but it must be started early enough for the servicer to review the file, issue any required approvals, evaluate the buyer’s offer, and postpone or avoid the foreclosure sale when appropriate.

In California, the nonjudicial foreclosure process can move quickly once formal notices are recorded. A Notice of Default begins the formal foreclosure process, and the homeowner generally has a 90-day period to cure the default. After that, a Notice of Sale may be recorded, and the sale date can be scheduled after the legally required notice period.

If you have received a Notice of Default, Notice of Trustee Sale, or any letter stating that a sale date has been scheduled, contact us immediately. Waiting until the last minute can limit your options.

FHA Short Sale Relocation Assistance

Some eligible FHA homeowners may receive relocation or transition assistance through the FHA Pre-Foreclosure Sale program. This is not guaranteed and depends on the specific file, HUD/FHA requirements, servicer approval, cash reserve contribution requirements, junior liens, and final approval terms.

Short Sale relocation assistance should never be assumed until it is confirmed in writing. The short sale approval letter should be reviewed carefully before closing so you understand whether relocation assistance is approved and how it will be handled.

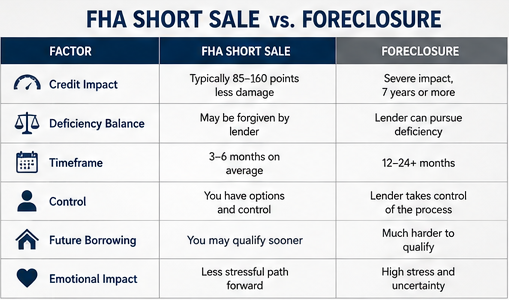

FHA Short Sale vs. Other Foreclosure Alternatives

A short sale is only one possible option. The right strategy depends on your income, hardship, property value, loan balance, timeline, and whether you want to keep or leave the home.

| Option | Best For | Main Consideration |

|---|---|---|

| Loan Modification | Homeowners who want to keep the home and may be able to afford a modified payment. | You need to qualify based on income, hardship, loan rules, and servicer guidelines. |

| FHA Short Sale | Homeowners who need to sell but owe more than the home is worth. | Requires servicer approval, HUD/FHA review, buyer approval, and proper documentation. |

| Deed in Lieu of Foreclosure | Homeowners who cannot complete a short sale and may be able to voluntarily transfer the property back. | The lender may require the property to be marketed first, and junior liens can create issues. |

| Foreclosure | Usually the last resort when no workout, sale, or settlement option is completed. | Can create serious credit, housing, timing, and legal consequences. |

| Traditional Sale | Homeowners who have enough equity to pay off the loan and closing costs. | If there is not enough equity, a short sale may need to be considered instead. |

Will FHA Forgive the Remaining Balance After a Short Sale?

In many approved FHA short sales, the remaining FHA mortgage balance may be settled through the approved transaction, but the approval letter must be reviewed carefully before closing. The exact language matters. Some files may involve cash contributions, junior lien negotiations, or other approval conditions.

There may also be tax consequences when mortgage debt is forgiven or settled for less than the full amount owed. You should speak with a qualified tax professional or attorney regarding your specific situation.

For more information, read our guide on what happens to the balance after a short sale.

Can I Get Another FHA Loan After a Short Sale?

Many borrowers may need to wait before qualifying for another FHA loan after a short sale, especially if the prior mortgage was delinquent. FHA waiting periods and exceptions depend on the borrower’s circumstances, credit history, whether the borrower was in default, and current FHA/lender underwriting requirements.

If your goal is to buy again after the short sale, speak with a qualified mortgage professional before closing so you understand the possible waiting period and what documentation you should keep.

You can also review our guide on buying after a short sale.

Why Work With San Diego Short Sale Experts?

FHA short sales involve more than listing a home and waiting for an offer. The process can include servicer communication, HUD/FHA guidelines, property value disputes, foreclosure timing, document deadlines, buyer screening, lien negotiations, and review of the short sale approval letter.

San Diego Short Sale Experts helps homeowners with:

- Reviewing whether an FHA short sale may be realistic

- Explaining short sale, loan modification, deed in lieu, and foreclosure alternatives

- Preparing the FHA short sale package

- Coordinating documents and authorization forms

- Pricing and marketing the property correctly

- Responding to servicer and negotiator requests

- Managing buyer offers and approval deadlines

- Helping resolve junior liens, HOA issues, and title concerns

- Coordinating with escrow, title, buyers, and the lender through closing

We serve homeowners throughout San Diego County and California who are facing foreclosure, underwater mortgages, FHA loan hardship, and other distressed property situations.

Expert Review

This page was reviewed by Glen Henderson, California real estate broker and short sale specialist, DRE #01384181. San Diego Short Sale Experts helps California homeowners evaluate short sale and foreclosure alternatives.

FHA Loan Short Sale FAQ

Can I short sale my FHA loan?

Yes, you may be able to short sale an FHA loan if the property is underwater, you qualify under FHA/HUD short sale guidelines, and your loan servicer approves the transaction. The FHA version of a short sale is often handled through HUD’s Pre-Foreclosure Sale program.

What is an FHA Pre-Foreclosure Sale?

An FHA Pre-Foreclosure Sale, or PFS, is HUD’s short sale program for eligible FHA-insured loans. It allows a homeowner to attempt to sell the property before foreclosure even when the sale price is less than the full amount owed.

Do I have to be behind on payments to do an FHA short sale?

Many FHA short sale files involve missed payments or default, but you should not intentionally miss payments without first getting advice from your servicer and qualified professionals. FHA short sale eligibility depends on the specific facts of your loan, hardship, and servicer review.

How long does an FHA short sale take?

Many FHA short sales take several months from initial review to closing. The timeline depends on how quickly the file is prepared, whether foreclosure is pending, how the property value comes in, whether a qualified buyer is found, and whether there are other liens or title issues.

Can an FHA short sale stop foreclosure?

An FHA short sale may help stop foreclosure if the file is started early enough and the servicer agrees to review or postpone the sale while the short sale is being processed. A short sale should not be treated as an automatic foreclosure stop, especially if a trustee sale date is close.

Can I receive relocation assistance after an FHA short sale?

Some eligible FHA homeowners may qualify for relocation or transition assistance through the FHA Pre-Foreclosure Sale program. The amount and eligibility depend on the file and must be confirmed in the written approval terms.

Does FHA forgive the shortage after a short sale?

The FHA mortgage balance may be resolved through an approved short sale, but the approval letter must be reviewed carefully. Junior liens, tax issues, cash contributions, and deficiency language should be reviewed before closing.

What documents are needed for an FHA short sale?

Common documents include a hardship explanation, income documentation, bank statements, tax documents if requested, mortgage information, authorization forms, listing agreement, purchase contract, buyer pre-approval or proof of funds, and an estimated settlement statement.

Can I get another FHA loan after a short sale?

Possibly, but many borrowers must wait before qualifying for another FHA loan, especially if the prior mortgage was delinquent. The waiting period and exceptions depend on FHA rules, lender overlays, credit history, and the facts surrounding the short sale.

Should I choose a short sale, loan modification, deed in lieu, or foreclosure?

The right option depends on whether you want to keep the home, whether you can afford a modified payment, how much the property is worth, how much is owed, whether foreclosure has started, and whether there are other liens. A short sale is often worth exploring when you need to sell but do not have enough equity to pay off the FHA loan in full. A deed in lieu is typically a last resort after you have attempted a short sale. A loan modification will only be an option if you still have steady income and can show that you are able to continue making payments.

Sources

- HUD: FHA Loss Mitigation Program

- HUD Form 90035: Pre-Foreclosure Sale Procedure Information Sheet

- HUD: FHA Single Family Housing Policy Handbook 4000.1

- California Courts: Your Rights in a Nonjudicial Foreclosure

- HUD: Find a HUD-Approved Housing Counselor

Find Out If You Qualify for an FHA Short Sale

If you have an FHA loan, owe more than your home is worth, or are worried about foreclosure, the best time to review your options is before deadlines become urgent. We can help you understand whether an FHA short sale may be an option and what steps may be needed next.

There is no cost or obligation to speak with us.