What Is Going to Happen With Foreclosures In 2021?

A leading economist is warning that this year’s booming housing market will soon give way to a rising tide of foreclosures that will submerge many homeowners in the coming year.

In an opinion piece published on Bloomberg, Michael R. Strain, the John G. Searle Scholar and the director of economic policy studies at the American Enterprise Institute (AEI) observed that while existing homes increased by 9.4% in September to 6.6 million units on an annual basis – the highest level in more than 14 years – and the median existing-home price was 14.8% higher in September versus one year earlier, this demand has been fueled by limited supply and historically low mortgage rates.

“The housing sector is relatively sensitive to interest rates, and mortgage costs — already low before the pandemic began — are at rock bottom, driven to current lows by the Federal Reserve’s rate cuts and asset purchases,” Strain wrote. “As of Oct. 22, the average 30-year fixed-rate mortgage was 2.8%, down from 3.75% a year before. Fifteen-year fixed-rate mortgages have been below 2.75% since the beginning of May.”

The COVID-19 pandemic also complicated the picture. With greater housing, people became eager for more living space. However, the supply of new houses has dwindled – Strain noted AEI Housing Center estimated there was only slightly more than two months’ worth of housing inventory in September.

The problem, Strain forecasted, was a so-called “K-shaped” recovery that will benefit wealthier Americans but leave lower-income households behind.

“Weak labor markets are typically a headwind for the housing sector,” he continued. “But job losses have been concentrated among low-wage workers who are less likely to purchase houses. The unemployment rate for college graduates is 4.8%, considerably lower than the overall rate of 7.9%.”

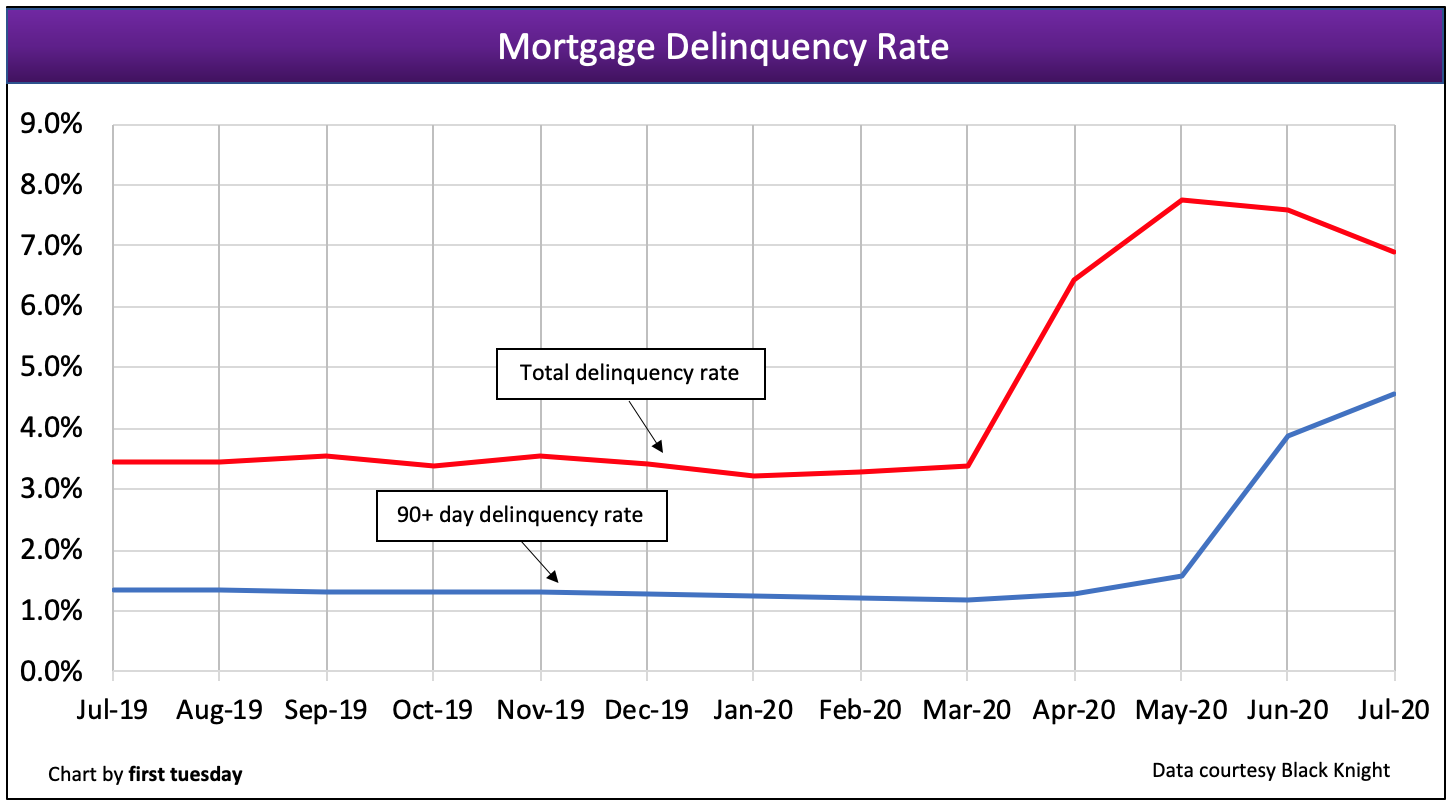

As a result, he continued, a “wave of foreclosures is likely coming that will hit low-income homeowners. As of August, over 10% of the eight million single-family mortgages backed by the Federal Housing Administration were delinquent by more than three months. According to the FHA, the reason for 86% of those delinquencies was ‘a national emergency,’ a category that includes the pandemic. These delinquencies are heavily concentrated among loans associated with low credit scores.”

While federal forbearance policies put a temporary freeze on foreclosures—only 352 foreclosures were started in August, compared with 10,438 in February—Strain commented that policy would not remain in place next year.

An important explanation for why there are so few foreclosures amid so many delinquencies can be found in the Cares Act, the economic recovery law passed in March. It included forbearance provisions that allowed borrowers with government-backed mortgages to postpone (or reduce) payments for up to 12 months if they suffered Covid-related financial hardship.

When these forbearance provisions expire in 2021, expect a wave of foreclosures to follow.