Are Short Sales Increasing in 2026? What Homeowners Need to Know About Short Sales, Foreclosures, and VA Loan Short Sales

After several years of historically low foreclosure activity, many homeowners, real estate professionals, and investors are starting to ask the same question: Are short sales increasing again?

The answer is more nuanced than a simple yes or no.

At the national level, short sales are still not happening at the level we saw during the housing crisis. Most homeowners still have equity, and distressed sales remain a very small percentage of total home sales. However, several warning signs are starting to appear. Foreclosure filings are increasing, more homeowners are falling behind on their mortgage payments, and the number of underwater homeowners has started to rise in certain markets.

For homeowners who need to sell but owe more than their home is worth, a short sale may once again become an important option to understand.

This is especially true for homeowners with VA loans, FHA loans, or other low-down-payment loans. These borrowers may have less equity cushion if home values decline or if they need to sell sooner than expected.

If you are unfamiliar with the process, you can start with our guide explaining what a short sale means in real estate.

What Is a Short Sale?

A short sale happens when a homeowner sells a property for less than the total amount needed to pay off the mortgage, closing costs, real estate commissions, escrow fees, title fees, and any other liens or selling expenses.

In a normal sale, the homeowner has enough equity to pay everything off at closing. In a short sale, there is not enough equity, so the lender must approve the sale and agree to accept less than the full amount owed.

For example, a homeowner may owe $520,000 on a property, but the home may only be worth $500,000. After commissions, closing costs, unpaid HOA dues, taxes, and other fees, the seller may be “short” by tens of thousands of dollars. Instead of bringing that money to closing, the homeowner may be able to ask the lender to approve a short sale.

A short sale can help a homeowner avoid foreclosure, but it must be handled correctly. The lender will review the homeowner’s financial hardship, the property value, the purchase offer, and the expected loss before deciding whether to approve the sale.

You can also review our page on alternatives to foreclosure if you are trying to compare short sales, loan modifications, repayment plans, and other options.

What the Latest Data Says About Short Sales

Based on the most recent available public data, there is not yet a major nationwide wave of closed short sales. Distressed sales, which include both foreclosures and short sales, remain a small share of total existing-home sales.

In April 2026, distressed sales represented approximately 2% of existing-home sales nationwide. That figure was unchanged from the prior month and unchanged from the prior year.

That tells us something important: short sales are not yet a major share of the national housing market.

However, closed short sales are a lagging indicator. A short sale usually happens only after several conditions come together:

- The homeowner experiences a financial hardship.

- The homeowner falls behind or is at risk of falling behind.

- The home cannot be sold for enough to pay off all liens and selling costs.

- The lender agrees to approve the short payoff.

That means the better early warning signs are foreclosure filings, delinquency rates, and negative equity. In those categories, the data is more concerning.

Foreclosure Activity Is Increasing From Recent Lows

According to ATTOM’s 2025 U.S. foreclosure data, foreclosure activity increased in 2025 compared with 2024. ATTOM reported that 367,460 U.S. properties had foreclosure filings in 2025, up 14% from the prior year. Foreclosure starts also increased, and completed foreclosures rose as well.

You can review ATTOM’s full foreclosure report here: ATTOM 2025 U.S. Foreclosure Market Report.

This does not mean we are back in a 2008-style housing crisis. We are not. Foreclosure activity is still far below the levels seen during the Great Recession.

But the direction matters.

When foreclosure activity rises, more homeowners begin looking for ways to avoid foreclosure. For some, a loan modification may be the best solution. For others, selling may be the only realistic option. If the property cannot sell for enough to cover the full mortgage balance and costs of sale, a short sale may become the best alternative.

Negative Equity Is Also Rising in Some Markets

A homeowner is considered underwater when they owe more on the mortgage than the home is worth. A homeowner may also be functionally underwater if they technically have some equity but not enough to cover commissions, closing costs, unpaid taxes, HOA fees, and other expenses required to sell.

This is important because short sales usually require two key ingredients: financial hardship and lack of equity.

Recent home equity reports show that negative equity remains low nationally, but it has been increasing. Cotality reported that negative equity rose year over year to approximately 1.1 million homes, or about 2% of mortgaged properties. ATTOM also reported that seriously underwater mortgage rates remain relatively low nationally but are higher in certain states, especially in parts of the South and Midwest.

The states with some of the highest seriously underwater rates include Louisiana, Mississippi, Kentucky, Iowa, and Arkansas. Other areas with rising foreclosure or equity pressure include parts of Florida, Nevada, Texas, Arizona, and California.

For California homeowners, the risk is often different than in lower-priced markets. Many California homeowners still have substantial equity because of long-term appreciation. However, recent buyers who purchased near the top of the market with little or no money down may be more vulnerable if they need to sell quickly.

Why VA Loan Short Sales Deserve Special Attention

VA loans are one of the most important categories to watch when discussing future short-sale activity.

A VA loan is a powerful benefit for eligible Veterans, active-duty service members, and surviving spouses. One of the major advantages is that many VA buyers are able to purchase with little to no down payment. That can be extremely helpful when buying a home, but it also means that some VA borrowers may have less equity if they need to sell shortly after purchasing.

A VA loan short sale is often called a VA compromise sale. This happens when a Veteran or VA borrower sells the home for less than the full amount owed and the lender or servicer accepts a short payoff.

We have a full guide on VA loan short sales and VA compromise sales that explains how the process works.

VA loan short sales are especially important because the borrower may need to understand:

- Whether the VA will approve the compromise sale

- How the short sale may affect future VA loan eligibility

- Whether any remaining entitlement will be impacted

- Whether there could be a deficiency issue

- Whether the borrower may qualify for other foreclosure-avoidance options first

The U.S. Department of Veterans Affairs also lists short sales as one of the possible options for borrowers who are having trouble making payments. You can review VA’s homeowner assistance guidance here: VA help to avoid foreclosure.

Is There Public Data on the Number of VA Short Sales?

This is where the data becomes more limited.

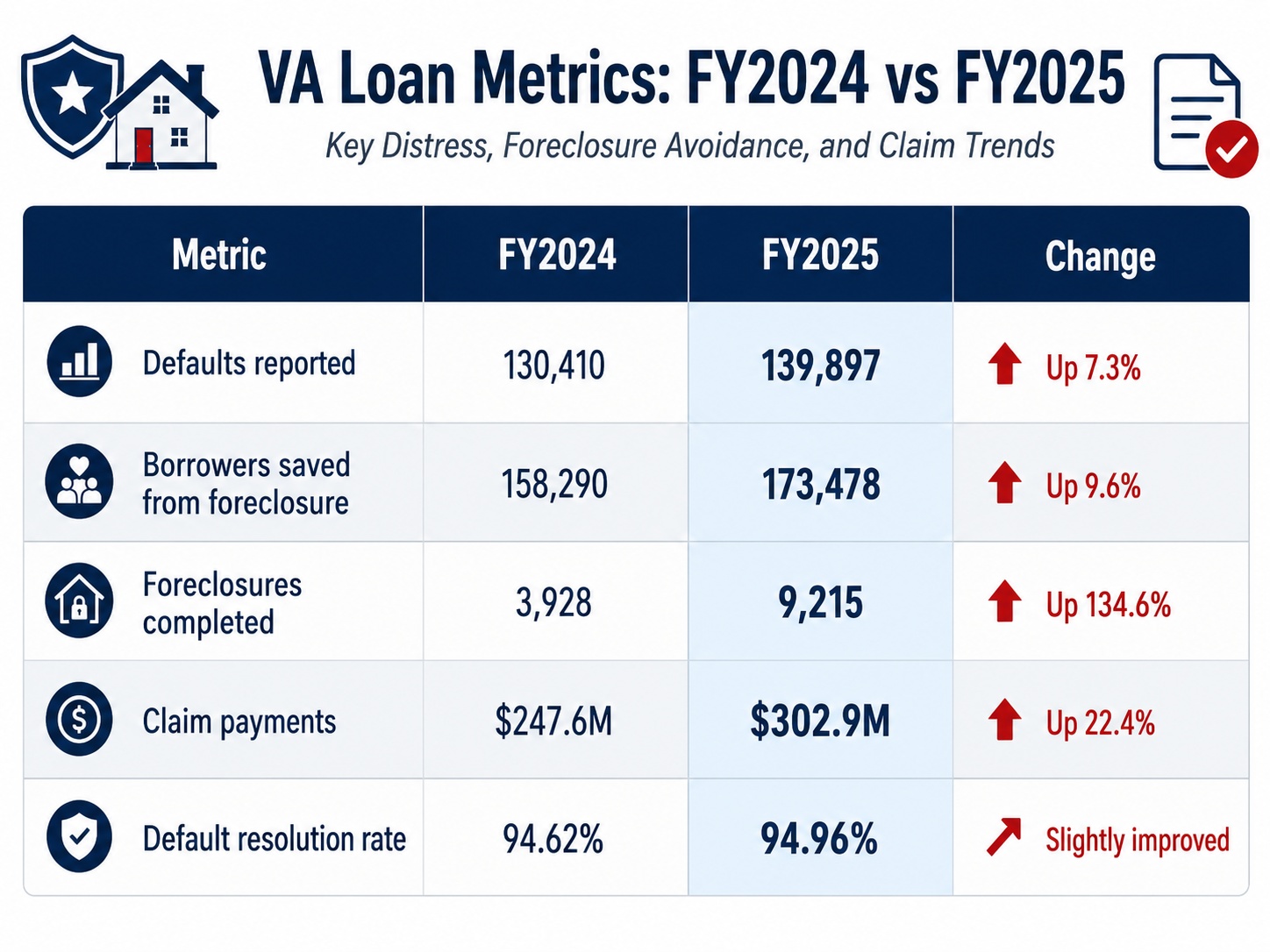

There is strong public data on VA loan volume, VA defaults, VA foreclosure completions, and VA claim payments. However, publicly available VA reports do not clearly break out the exact number of VA compromise sales or the total amount forgiven through VA short sales.

That means we can track the larger distress trend in VA loans, but we cannot easily identify the exact number of closed VA short sales nationwide from public data alone.

What we do know is that VA loan distress increased in several important areas. VA’s FY2025 Loan Guaranty data showed an increase in reported defaults, completed foreclosures, and claim payments compared with FY2024. VA also reported helping a large number of borrowers retain homeownership or avoid foreclosure.

That suggests that VA loan distress is an area worth watching closely, even if VA short-sale-specific numbers are not easily available to the public.

Why VA Borrowers May Be More Exposed in a Shifting Market

VA loans are not “bad loans.” In fact, VA loans are one of the best mortgage programs available for eligible borrowers. The concern is not the loan program itself. The concern is the combination of several market conditions:

- Many VA buyers purchase with little or no down payment

- Some recent buyers purchased when prices and interest rates were high

- Homeowners who purchased recently may not have had enough time to build equity

- Selling costs can quickly erase a small equity position

- Military relocation, divorce, job loss, disability, or income changes can force a sale

- Higher insurance, taxes, HOA dues, and living costs can create payment stress

In a rising market, these risks are often hidden because appreciation builds equity quickly. In a flat or declining market, the risks become more visible.

A Veteran may not be deeply underwater based only on the mortgage balance, but once closing costs and selling expenses are added, the seller may not have enough equity to close. That is when a VA compromise sale may become necessary.

Are Short Sales Increasing in California?

California is not currently seeing a broad short-sale wave like the one experienced after the housing crash. Many homeowners still have significant equity, especially those who purchased before the recent run-up in prices.

However, California has several conditions that could increase short-sale pressure in specific situations:

- High home prices

- Higher mortgage payments for recent buyers

- Higher property taxes and insurance costs

- Elevated HOA dues in some condo communities

- Slower buyer demand in some price ranges

- Longer market times in certain areas

- Recent buyers with limited equity

- Homeowners who need to sell because of hardship or relocation

In San Diego County, most homeowners are still protected by equity. But short sales can still happen when a homeowner purchased recently, used a low-down-payment loan, refinanced heavily, experienced a hardship, or needs to sell before appreciation has created enough equity.

For homeowners in this situation, timing matters. The earlier you evaluate your options, the more choices you may have.

Short Sale vs. Foreclosure: Why Acting Early Matters

Many homeowners wait too long to ask for help because they are embarrassed, overwhelmed, or hoping the situation will improve on its own. Unfortunately, waiting can reduce the number of available options.

A short sale is usually easier to pursue before the foreclosure process gets too far along. Once a foreclosure sale date is scheduled, timing becomes more difficult. The lender may still consider a short sale, but the approval process can take time, and the foreclosure timeline may continue moving forward.

A successful short sale requires coordination between the homeowner, real estate agent, buyer, lender, servicer, escrow, title, and any junior lienholders. If there are HOA liens, tax liens, second mortgages, solar liens, or other claims against the property, those issues must also be addressed.

That is why working with an experienced short-sale team matters.

You can learn more about our approach on our What We Do and Don’t Do page.

How Much Does a Short Sale Cost?

In many short-sale situations, the lender-approved closing statement includes the real estate commissions, escrow fees, title fees, and other normal selling costs. That means the homeowner may not have to pay these expenses out of pocket, depending on the lender approval and the specifics of the file.

Every situation is different. The final terms depend on the lender, investor guidelines, property value, offer price, liens, hardship, and approval letter.

For a more detailed breakdown, review our guide on how much a short sale costs.

What Areas Are Most Likely to See More Short Sales?

The areas most likely to see an increase in short sales are not necessarily the areas with the highest home prices. The bigger risk factors are affordability pressure, recent price declines, high foreclosure activity, and a larger share of low-equity homeowners.

Markets to watch include:

- States with higher foreclosure rates

- Areas where insurance and taxes have increased sharply

- Markets where home values have softened after rapid appreciation

- Areas with a high concentration of recent FHA or VA buyers

- Military-heavy markets where relocations can force sales

- Condo-heavy markets with rising HOA dues or special assessments

For VA loans specifically, short-sale risk may be more concentrated in military markets where borrowers purchased recently with little or no down payment and now need to sell because of relocation, income changes, divorce, or hardship.

What Should a Homeowner Do If They Think They May Need a Short Sale?

If you owe more than your home is worth, or you are not sure if you have enough equity to sell, the first step is to get a realistic estimate of your property value and payoff numbers.

You will want to gather:

- Your current mortgage balance

- Any second mortgage or HELOC balances

- HOA dues or unpaid assessments

- Property tax status

- Estimated market value

- Estimated selling costs

- Any foreclosure notices or sale dates

- Details about your hardship

From there, an experienced short-sale professional can help determine whether a traditional sale, loan modification, repayment plan, forbearance, deed-in-lieu, or short sale may be the best path.

The most important thing is to act before the situation becomes urgent.

If you are in San Diego County or anywhere in California and need help evaluating your options, you can contact San Diego Short Sale Experts for a confidential, no-obligation consultation.

Final Thoughts: Short Sales Are Not Back Everywhere, But Risk Is Rising

Short sales are not flooding the market in 2026. Distressed sales remain a small percentage of total home sales, and most homeowners still have equity.

However, the early warning signs are becoming harder to ignore. Foreclosure filings are up, mortgage delinquencies have increased, negative equity has grown in some markets, and VA loan distress deserves close attention.

For homeowners with VA loans, recent purchases, low equity, or financial hardship, a short sale may become an important option to understand. A short sale is not the right solution for every homeowner, but it can be a powerful alternative to foreclosure when there is not enough equity to sell traditionally.

If you are worried about falling behind, facing foreclosure, or selling a home that may not have enough equity, do not wait until the last minute. The sooner you understand your options, the more control you may have over the outcome.

Frequently Asked Questions About Short Sales in 2026

Are short sales increasing in 2026?

Short sales are not yet showing a major national increase as a share of total home sales. However, foreclosure filings, delinquencies, and negative equity have increased in some areas, which could lead to more short-sale activity if homeowners need to sell without enough equity.

What is the difference between a short sale and a foreclosure?

A short sale is when the homeowner sells the property with lender approval for less than the full amount owed. A foreclosure is when the lender takes legal action to repossess and sell the property after the borrower defaults. A short sale may give the homeowner more control than allowing the home to go through foreclosure.

Can you do a short sale with a VA loan?

Yes. A VA loan short sale is commonly called a VA compromise sale. The lender, servicer, and VA guidelines must be followed, and the borrower should understand how the short sale may affect future VA loan entitlement.

Will a VA short sale affect my ability to use a VA loan again?

It may. A VA compromise sale can affect the borrower’s remaining VA entitlement, depending on the loss and whether the VA pays a claim. However, some Veterans may still be able to use remaining entitlement or restore entitlement in the future. This should be reviewed carefully before moving forward.

Do I have to be behind on payments to do a short sale?

Not always. Some lenders may consider a short sale if there is a documented hardship and the homeowner cannot sell for enough to pay off the loan and costs of sale. However, each lender and investor has different rules.

How long does a short sale take?

The timeline can vary. Some short sales are approved in a few months, while more complicated files can take longer. Multiple liens, HOA issues, foreclosure timelines, buyer delays, or incomplete documentation can all affect the process.

Who should I contact if I need help with a short sale in San Diego?

You can contact San Diego Short Sale Experts for help reviewing your options. There is no cost or obligation to ask questions and understand whether a short sale, loan modification, repayment plan, or another option may make sense for your situation.

“`