VA Loan Foreclosure: What to Do If Your VA Loan Is in Foreclosure

If you have a VA loan in foreclosure, you may still have options. Depending on your situation, you may be able to stop foreclosure, catch up on missed payments, request mortgage assistance, sell the home before the auction, or complete a VA short sale before the foreclosure is finalized.

At San Diego Short Sale Experts, we help homeowners and Veterans understand their options, communicate with the mortgage servicer, prepare short sale documentation, negotiate with the lender, and work toward a solution before the foreclosure sale date.

Need Help With a VA Loan in Foreclosure?

If you are behind on payments, facing foreclosure, have received a Notice of Default, or have a trustee sale date scheduled, contact us today. We can review your situation, explain your options, and help determine whether you may qualify for a VA short sale, foreclosure delay, loan modification, or another solution.

There is no cost or obligation to speak with us.

Quick Answer: What Are Your Options With a VA Loan in Foreclosure?

If your VA loan is in foreclosure, your main options may include a repayment plan, special forbearance, VA loan modification, VA Partial Claim, extra time to arrange a private sale, VA short sale, or deed in lieu of foreclosure. The best option depends on your hardship, income, missed payments, equity, foreclosure timeline, and whether you want to keep or sell the home.

Bottom line: A VA loan foreclosure does not always mean you will lose the home, but the earlier you act, the more options you may have.

Understanding the VA Loan Foreclosure Process

A VA loan foreclosure happens when a homeowner falls behind on a VA-guaranteed mortgage and the mortgage servicer begins the legal process to take back and sell the property. Even though the loan is backed by the Department of Veterans Affairs, the day-to-day servicing is usually handled by a private mortgage company.

If your VA loan is in foreclosure, it is important to understand that foreclosure is a process, not a single event. In many cases, there may still be time to review options before the home is sold at auction. The key is to act quickly, communicate with the servicer, and determine whether your goal is to keep the home or sell it before foreclosure.

If you are trying to understand how a foreclosure compares to selling before the auction, read our guide on short sale vs. foreclosure.

What to Do If Your VA Loan Is in Foreclosure

If your VA loan is in foreclosure, the first step is to confirm where you are in the foreclosure timeline and contact your mortgage servicer immediately. Waiting too long can reduce your options, especially if a trustee sale date has already been scheduled.

Important first steps:

- Contact your mortgage servicer immediately. Ask for the loss mitigation or mortgage assistance department.

- Contact the VA Home Loan program. VA loan technicians may be able to help you understand your options. The VA Home Loan number is 877-827-3702.

- Find out where you are in the foreclosure timeline. If you are in California, review the California foreclosure timeline.

- Review any foreclosure notices you have received. If you received a Notice of Default, read our guide on what a Notice of Default means.

- Confirm whether a trustee sale date has been scheduled. If you received a Notice of Trustee’s Sale, read our guide on what a Notice of Trustee’s Sale means.

- Decide whether keeping the home is realistic. If the payment is no longer affordable, selling or pursuing a VA short sale may be the better option.

- Speak with a short sale specialist early. If you owe more than the home is worth, a VA short sale or VA compromise sale may be an option.

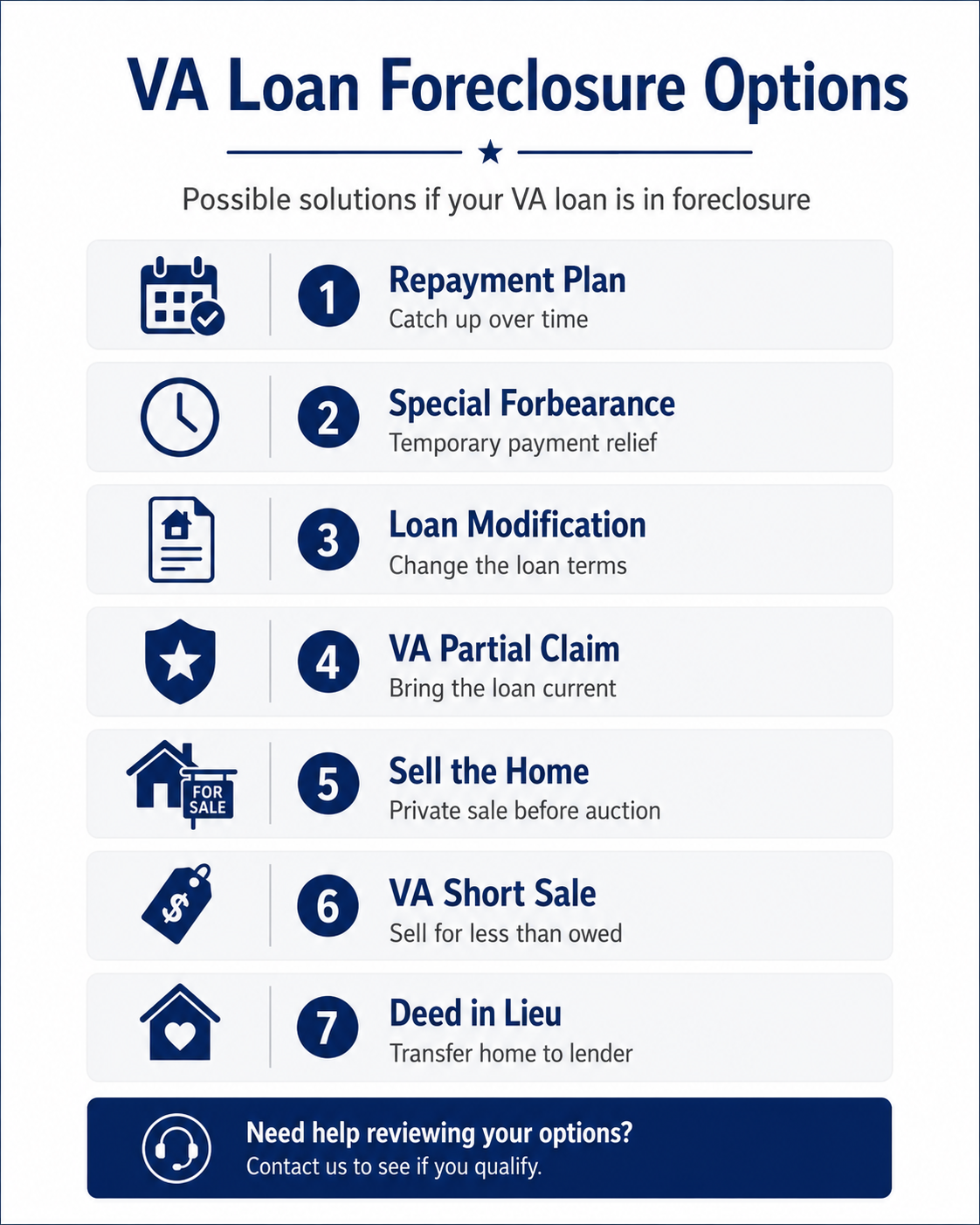

VA Loan Foreclosure Options

The right VA loan foreclosure option depends on whether you want to keep the home or sell it before foreclosure. Some options are designed to help you keep the property, while others are designed to help you avoid foreclosure by selling or transferring the property before the foreclosure is completed.

1. Repayment Plan

A repayment plan may work if your hardship was temporary and you can afford your normal monthly mortgage payment plus an additional amount each month to catch up on the missed payments. This option is usually more realistic when the delinquency is smaller and your income has recovered.

2. Special Forbearance

Special forbearance may give you extra time to repay missed payments after a temporary hardship. Forbearance does not erase the missed payments. You will still need a plan for what happens when the forbearance period ends.

3. VA Loan Modification

A VA loan modification may be an option if you need a new payment structure. In many cases, a modification adds missed payments and certain costs to the loan balance and creates a new payment schedule. This may help some homeowners keep the property, but the modified payment still needs to be affordable long term.

You can also review our related guide on loan modification options.

4. VA Partial Claim

The VA Partial Claim program may help certain eligible VA borrowers bring a delinquent loan current. In general, this option allows the VA to work with the mortgage servicer to cover the amount needed to bring the loan current, with repayment due later when the loan is paid off or the home is sold.

Important 2026 update: VA says the Partial Claim program is open for submissions, but servicers have until November 28, 2026, to implement the program into their systems. Borrowers should contact their servicer to confirm availability and eligibility.

Before a borrower can receive a VA Partial Claim, the borrower may need to complete a successful trial payment plan. The borrower must work directly with the mortgage servicer to begin the Partial Claim process.

You can read more on the official VA page for VA help to avoid foreclosure.

5. Extra Time to Arrange a Private Sale

If you need to sell the home, the servicer may allow extra time to arrange a private sale. This can be helpful if the home is already listed, a buyer is ready, or escrow is already open and the sale needs more time to close.

If you have equity, a traditional sale may be the best way to avoid foreclosure. If you do not have equity, a VA short sale may be needed.

6. VA Short Sale

A VA short sale, also called a VA compromise sale, may be an option if you owe more than the home is worth and cannot afford to keep the property. In a VA short sale, the home is sold for less than the full loan balance, and the servicer reviews the hardship, offer, property value, title, estimated closing statement, and supporting documents before deciding whether to approve the sale.

Key takeaway: If you owe more than the home is worth and cannot afford to keep it, a VA short sale may be one of the main alternatives to foreclosure.

This can be one of the most important options for a homeowner with a VA loan in foreclosure when keeping the home is no longer realistic. Learn more in our full guide to VA loan short sales and VA compromise sales.

7. Deed in Lieu of Foreclosure

A deed in lieu of foreclosure means you voluntarily transfer the property back to the lender instead of going through a completed foreclosure. This may be an option when you cannot keep the home and a sale or short sale is not possible.

A deed in lieu can still affect credit, future VA loan entitlement, and your ability to buy again. It can also be more difficult if there are junior liens, HOA balances, judgments, or title problems. You can learn more about deed in lieu of foreclosure.

VA Loan Foreclosure Options Compared

| Option | Best For | Important Consideration |

|---|---|---|

| Repayment Plan | Temporary hardship and ability to pay extra each month | You must be able to afford the regular payment plus an additional catch-up amount. |

| Special Forbearance | Short-term hardship with expected recovery | Missed payments still need to be resolved after the forbearance period. |

| Loan Modification | Borrowers who need a new payment structure | The modified payment still needs to be affordable long term. |

| VA Partial Claim | Eligible borrowers who can resume payments after the arrears are addressed | You must work with your servicer and may need to complete a trial payment plan. |

| Traditional Sale | Homeowners with enough equity to pay off the VA loan | The sale must close before the foreclosure auction. |

| VA Short Sale | Homeowners who owe more than the home is worth | The servicer and VA must approve the sale. |

| Deed in Lieu | Last-resort exit when a sale is not possible | May affect credit and future VA loan entitlement. |

Which VA Foreclosure Option Fits Your Situation?

The best option depends on your income, hardship, equity, timeline, and whether you want to keep or sell the home. This table can help you think through the most common starting points.

| Your Situation | Option to Ask About |

|---|---|

| Your hardship was temporary and your income has recovered | Repayment plan or special forbearance |

| You want to keep the home but need a different payment structure | VA loan modification or VA Partial Claim |

| You need to sell and have enough equity to pay off the loan | Traditional sale before the foreclosure auction |

| You owe more than the home is worth and cannot afford the payment | VA short sale or VA compromise sale |

| You cannot keep the home, and a sale is not possible | Deed in lieu of foreclosure |

| You are an active-duty service member or have recently served | Ask about SCRA protections and speak with a qualified attorney |

Should You Try to Keep the Home or Sell Before Foreclosure?

Keeping the home may make sense if the hardship was temporary, your income has recovered, and the mortgage payment can be made affordable long-term. Selling may make more sense if the payment is no longer realistic, the foreclosure sale date is approaching, or you owe more than the property is worth.

| Keeping the Home May Make Sense If | Selling May Make Sense If |

|---|---|

| Your income has recovered | The payment is no longer affordable |

| The hardship was temporary | You need to relocate or cannot maintain the home |

| The servicer offers a workable repayment plan or modification | A loan modification was denied or is not realistic |

| You can afford the home after the arrears are resolved | You owe more than the home is worth |

| You have enough time to complete the servicer review | A Notice of Trustee’s Sale has been recorded |

VA Loan Foreclosure in California

In California, most residential foreclosures are handled through a nonjudicial foreclosure process, which usually includes a Notice of Default and a Notice of Trustee’s Sale before the property is sold at auction. If your VA loan is in foreclosure in California, timing is critical because a short sale, traditional sale, loan modification, or other solution generally needs to be reviewed before the trustee sale occurs.

If you have received a Notice of Trustee’s Sale, the foreclosure process has formally started. In addition, an auction date may already be scheduled. Review our California-specific resources on the California foreclosure timeline, Notice of Default, and Notice of Trustee’s Sale.

Important: If your sale date is close, do not wait. A complete short sale package, buyer offer, servicer review, and foreclosure postponement request can take time.

Can Active-Duty Military Members Get Additional Foreclosure Protection?

Some active-duty service members may have additional protections under the Servicemembers Civil Relief Act, commonly called SCRA. These protections may include certain foreclosure-related protections, interest rate protections, or other rights depending on the facts of the loan, the timing of service, and the borrower’s situation.

If you are active-duty military, recently served, or believe your military service may affect your foreclosure situation, speak with a qualified attorney or legal assistance office. We can help with the real estate and short sale side of the process, but we do not provide legal advice.

When a VA Short Sale May Make Sense

A VA short sale may make sense when you owe more than the home is worth, cannot afford the mortgage payment, and need to avoid a completed foreclosure. It may also be an option if keeping the home is not realistic and a traditional sale will not pay off the full loan balance.

A VA short sale may be worth exploring if:

- You have a VA loan in foreclosure.

- You owe more than the home is currently worth.

- You cannot afford the mortgage payment long term.

- A repayment plan, forbearance, loan modification, or Partial Claim is not realistic.

- You need to sell because of job loss, reduced income, divorce, medical issues, relocation, military orders, death in the family, increased expenses, or another hardship.

- You have received a Notice of Default or Notice of Trustee’s Sale.

- You want to avoid a completed foreclosure and maintain more control over the outcome.

A VA short sale is not automatic. The servicer will usually need a complete short sale package, a valid hardship, a qualified buyer, market documentation, title information, and an estimated settlement statement. If the file is incomplete or the property value is disputed, the short sale can be delayed or denied.

For a deeper explanation, read our guides on how the short sale process works and how to qualify for a short sale.

Can a VA Short Sale Stop Foreclosure?

In some cases, yes. A VA short sale may help avoid a completed foreclosure if the servicer reviews and approves the sale before the auction date. However, postponement is not guaranteed, and timing is critical.

In some situations, the servicer may postpone the foreclosure sale while a complete short sale package is under review. This is never guaranteed. The stronger the file, the sooner the package is submitted, and the more realistic the offer is, the better the chance of keeping the process moving.

If your sale date is close, review our guides on how to stop foreclosure now and ways to stop foreclosure immediately.

What Documents Are Usually Needed for a VA Short Sale?

Most VA short sale files require hardship documentation, financial documents, listing information, a buyer offer, title information, and a third-party authorization. The exact documents depend on the servicer, investor, foreclosure status, hardship, and whether there are other liens on the property.

In many VA short sale files, the servicer may request some or all of the following:

- Mortgage statement

- Hardship letter or hardship explanation

- Recent pay stubs or income documentation

- Recent bank statements

- Tax returns or other financial documents, if requested

- Listing agreement

- Purchase contract from a qualified buyer

- Buyer pre-approval letter or proof of funds

- Estimated settlement statement or closing statement

- HOA payoff, property tax information, or insurance information, if applicable

- Junior lien information, if there is a second mortgage, HELOC, judgment, tax lien, or other recorded lien

- Third-party authorization allowing your short sale negotiator or agent to communicate with the servicer

Do not submit incomplete or inaccurate paperwork. Missing documents, outdated bank statements, unsigned forms, or an unclear hardship explanation can delay the review and create problems as a foreclosure deadline approaches.

Download VA Foreclosure Assistance Documents and Resources

The VA does not use one single universal short sale application for every servicer. Your mortgage servicer may have its own loss mitigation application, financial worksheet, short sale package, and third-party authorization forms. However, the following official resources may help you understand your options if your VA loan is in foreclosure:

- VA Help to Avoid Foreclosure – Official VA page explaining foreclosure avoidance options for VA-backed loans.

- Download VA Veteran Borrowers in Delinquency Quick Reference Sheet PDF – VA document explaining common delinquency and foreclosure avoidance options.

- CFPB Guide to Avoiding Foreclosure Relief Scams – Consumer protection information about foreclosure rescue scams.

- CFPB Avoid Foreclosure Guide – Federal consumer guide explaining foreclosure prevention options.

Have Questions About Your Best Option?

The VA loan foreclosure process can be confusing, especially if you are trying to decide between a loan modification, VA Partial Claim, short sale, deed in lieu, or selling the home before the auction. We can help you understand the real estate side of the process and what documents may be needed if a VA short sale is the best option.

There is no cost or obligation to speak with us.

Why Work With VA Short Sale and Foreclosure Specialists?

A VA loan foreclosure can involve several moving parts, including the homeowner, mortgage servicer, VA, buyer, real estate agents, escrow, title, junior lienholders, HOA, and foreclosure trustee. If the home is underwater and a VA short sale is needed, the process can become even more time-sensitive.

Our job is to help organize the process, identify the available options, prepare the short sale file, communicate with the right parties, and work toward a solution before the foreclosure sale date whenever possible.

We help with:

- Reviewing your VA loan, hardship, foreclosure status, and property value

- Explaining options to keep the home or sell before foreclosure

- Helping determine whether a VA short sale may be realistic

- Preparing the short sale documentation package

- Pricing and marketing the property properly

- Securing and screening buyer offers

- Communicating with the servicer and assigned negotiator

- Coordinating escrow, title, buyer deadlines, and lien payoff issues

- Responding to document requests and valuation concerns

- Helping you avoid common short sale delays and mistakes

You can also learn more about our team and approach on our About Us page and our guide on why homeowners choose our team.

Expert Review

This page was reviewed by Glen Henderson, California real estate broker associate and short sale specialist, DRE #01384181. San Diego Short Sale Experts helps California homeowners evaluate short sale and foreclosure alternatives, including VA loan short sales and VA compromise sales.

Common VA Loan Foreclosure Challenges

VA foreclosure situations can become complicated because of timing, missing documents, valuation issues, servicer delays, title problems, multiple liens, HOA balances, or an upcoming trustee sale date. These issues should be addressed as early as possible.

Incomplete Mortgage Assistance Package

One of the most common causes of delay is an incomplete package. The servicer may need updated financials, signed forms, proof of income, bank statements, hardship details, a listing agreement, an offer, or a revised settlement statement before the review can continue.

Property Valuation Issues

If the servicer’s valuation comes in higher than the buyer’s offer, the servicer may counter the price or request additional market support. Proper pricing, comparable sales, repair documentation, photos, and buyer strength can be important.

Foreclosure Sale Date Pressure

A scheduled trustee sale date can make timing critical. If the foreclosure auction is close, the servicer may not have enough time to review a short sale unless the package is complete and submitted quickly. If you are facing an urgent sale date, contact us as soon as possible.

Junior Liens or HOA Balances

If there is a second mortgage, HELOC, judgment, tax lien, HOA lien, or other recorded lien, that party may also need to approve the short sale. Multiple approvals can make the negotiation more complex.

How a VA Foreclosure May Affect Future VA Loan Benefits

A completed foreclosure, short sale, or deed in lieu may affect future VA loan entitlement. In some cases, the VA may require repayment of the loss before full entitlement can be restored. Because every situation is different, Veterans should contact a VA loan technician at 877-827-3702 to understand how their specific situation may affect future eligibility.

You should also speak with a qualified tax professional or attorney about possible legal, tax, credit, and deficiency issues. We are not attorneys or tax advisors, but we can help with the real estate and short sale side of the process.

For more information about possible short sale balance issues, read our guide on what happens to the balance after a short sale.

Beware of VA Loan Foreclosure Scams

Homeowners facing foreclosure are often targeted by companies that promise unrealistic results, charge upfront fees, tell the homeowner to stop speaking with the lender, or pressure the homeowner to sign over title. Be careful with anyone who guarantees they can stop foreclosure or asks you to pay large upfront fees for foreclosure relief.

For more information, review the CFPB guide on how to spot and avoid foreclosure relief scams and our internal guide on short sale and foreclosure scams.

Frequently Asked Questions About VA Loan Foreclosure

Can you stop foreclosure on a VA loan?

Yes, it may be possible to stop or avoid foreclosure on a VA loan, depending on your situation and how far along the foreclosure process is. Options may include a repayment plan, special forbearance, loan modification, VA Partial Claim, private sale, VA short sale, deed in lieu, or other legal options.

What should I do if my VA loan is in foreclosure?

Contact your mortgage servicer immediately, contact VA Home Loans at 877-827-3702, gather your financial documents, review your foreclosure notices, and speak with a foreclosure or short sale specialist. If you are in California, confirm whether a Notice of Default or Notice of Trustee’s Sale has been recorded.

Can the VA help me avoid foreclosure?

VA loan technicians may be able to help you understand foreclosure avoidance options, and may help if you are having trouble working with your servicer. You should also continue working directly with your mortgage servicer because the servicer is usually responsible for reviewing mortgage assistance applications.

What is the VA Partial Claim program?

The VA Partial Claim program is a foreclosure avoidance option that may help eligible VA borrowers bring a delinquent loan current. The borrower must work with the mortgage servicer, and a successful trial payment plan will be required before approval.

Can I sell my home if my VA loan is in foreclosure?

Yes. In many cases, you can still sell the home before foreclosure. If the home has enough equity, a traditional sale may pay off the loan. If the home is worth less than the amount owed, a VA short sale or VA compromise sale may be an option.

What is a VA short sale?

A VA short sale, also called a VA compromise sale, allows a qualifying homeowner to sell the property for less than the full amount owed when the servicer and VA approve the transaction. It may be an alternative to foreclosure when the borrower cannot keep the home and the property is underwater.

Will a VA foreclosure affect my future VA loan benefit?

A completed foreclosure, short sale, or deed in lieu may affect future VA loan entitlement. Contact a VA loan technician at 877-827-3702 to understand how your specific situation may affect restoration of entitlement and future VA loan eligibility.

Is a deed in lieu better than foreclosure on a VA loan?

A deed in lieu may help avoid the formal foreclosure process, but it still means giving the property back to the lender and may affect credit and future VA loan eligibility. Typically, a deed in lieu is only considered after other options have been exhausted. (ie. loan modification, traditional sale, or short sale.)

Do I need an attorney if my VA loan is in foreclosure?

Some homeowners should speak with a foreclosure attorney, especially if there are legal disputes, bankruptcy questions, title issues, divorce, probate, military protections, tax concerns, or an imminent trustee sale date. We can help with the real estate and short sale side of the process, but we do not provide legal or tax advice.

Sources

- U.S. Department of Veterans Affairs: VA help to avoid foreclosure

- VA Veteran Borrowers in Delinquency Quick Reference Sheet PDF

- VA Home Loans Contact Information

- CFPB: Help for homeowners to avoid foreclosure

- CFPB: How to spot and avoid foreclosure relief scams

Talk to a VA Loan Foreclosure Specialist

If your VA loan is in foreclosure, do not wait until the last minute. Contact San Diego Short Sale Experts today. We can review your situation, explain your options, and help determine whether you may qualify for a VA short sale or another foreclosure alternative.

There is no cost or obligation to speak with us.